Received a Letter or Phone Call?

Received a Letter or Phone Call? Email Us

Email Us

Key Takeaways

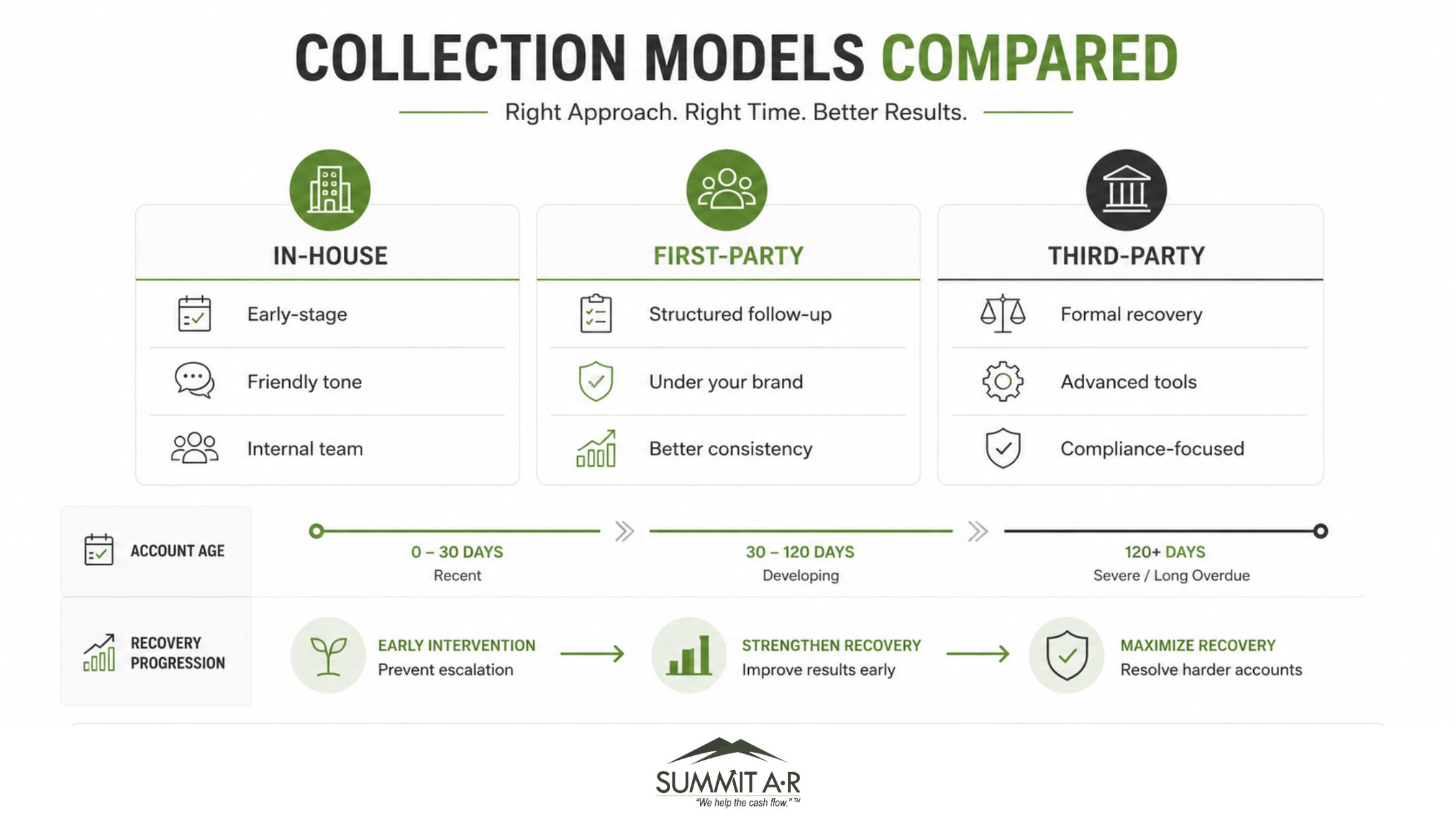

- “In-house” collections are handled by a creditor’s own accounts receivable team, while “first-party” collections are defined in the industry as debt recovery by a collection agency acting in the creditor’s name.

- “Third-party” collections are when a creditor outsources recovery to an agency that communicates in its own name.

- The right collection approach depends on factors like account age, customer communication history, internal resources, and recovery complexity.

- Collection agencies provide specialized tools, compliance expertise, and scalable recovery systems that many businesses can’t maintain internally.

- Consumer debt collection is heavily regulated at both the federal and state levels, making compliance a critical part of any recovery strategy.

- Modern collection strategies focus on ethical communication, technology-driven efficiency, and protecting brand reputation alongside financial recovery.

Consumer collections can feel simple from the outside: a balance is unpaid, so someone follows up. In practice, the way that follow-up happens can affect recovery speed, customer trust, compliance risk, staff workload, and your organization’s reputation. That is why the difference between in-house, first-party, and third-party collection support matters. Each model has a different role, and knowing when to use the right one helps you recover more revenue without asking your internal team to carry work it may not be built to handle.

Definitions of First-Party and Third-Party Collections

Before comparing consumer collections strategies, it helps to clear up the language. “First-party” and “third-party” are often defined online by their literal definitions, not those used in the industry, which are based on the federal Fair Debt Collection Practices Act (FDCPA). The distinction comes down to whose name is being used when the consumer is contacted.

What “In-House” Collections Means

In-house collections are the creditor’s own efforts to recover unpaid balances. In other words, your organization’s internal accounts receivable team, billing department, office administrator, customer service staff, or finance team is handling the follow-up directly.

This usually happens early in the payment cycle. Your team may send reminders, make calls, answer billing questions, confirm insurance or payment details, or offer a reasonable path to bring the account current. In-house collections can work well when the account is only slightly past due and the consumer is still responsive.

The challenge is that in-house teams are rarely dedicated only to collections. They may also be processing payments, supporting customers, managing invoices, coordinating with operations, or handling daily administrative issues. When overdue accounts pile up, follow-up becomes inconsistent. That inconsistency can quickly turn collectible accounts into harder recoveries.

What “First-Party” Collections Means

First-party collections, in the way we use the term for our collection services, happen when our team works in the creditor’s name. The consumer-facing communication appears to come from your organization, even though a professional agency is supporting the process behind the scenes.

This can be a strong fit when you want more structure, better technology, and more consistent follow-up, but you still want the communication to feel like an extension of your own billing or accounts receivable process. The consumer recognizes the creditor’s name, and the tone can stay service-oriented while the collection effort becomes more organized and productive.

First-party support is especially useful for early intervention. Instead of waiting until an account is old, disputed, or difficult to locate, your organization can bring in trained recovery support while there is still a better chance of cooperation.

What “Third-Party” Collections Means

Third-party collections happen when a creditor outsources recovery to an agency, and the agency communicates in its own name. At this stage, the consumer understands that a separate collection agency is now involved in the recovery process.

A professional agency brings trained collectors, documented workflows, compliance systems, account prioritization tools, skip tracing, and often credit reporting options that many internal teams simply don’t have.

This doesn’t mean the process has to feel aggressive. Reputable agencies, including Summit, handle third-party recovery with professionalism, respect, and strong brand awareness. The goal is not to pressure people unnecessarily, but to create a realistic, clear, and consistent path toward resolution.

How First- and Third-Party Collection Models Compare

Early on, a message from the creditor’s name may feel familiar and less formal. Later, when an account has gone unresolved, communication from a collection agency can signal that the matter now needs more serious attention.

When Each Approach Is Usually Used

In-house collections often start immediately after a missed payment. First-party support is commonly used when a creditor wants to strengthen early-stage recovery without making the account feel like it has fully escalated. Third-party collections usually come later, once the account needs a more formal recovery process.

The timing should not be random. Waiting too long can reduce recovery potential, especially if contact information becomes outdated or the consumer’s financial situation changes. On the other hand, escalating too quickly can create unnecessary friction. A smarter strategy matches the collection approach to account age, consumer responsiveness, balance size, and internal capacity.

How the Tone and Process Change

In-house outreach often sounds closer to customer service. The message may focus on a missed payment, a billing question, a payment arrangement, or a reminder that the account needs attention.

First-party and third-party recovery is typically more structured. Communications are documented carefully, account activity is tracked, compliance requirements are monitored, and follow-up happens according to a defined workflow. That structure is one of the reasons businesses outsource consumer collections when their own teams can no longer manage accounts consistently.

Benefits and Limitations of Each Approach

No single collection model is right for every account. A healthy recovery strategy usually uses the right level of intervention at the right time.

Benefits of In-House Collections

In-house collections give your organization direct control over messaging and customer experience. Your team already knows the account history, the consumer relationship, and any service or billing context that may affect the conversation.

This can be helpful when the issue is simple, recent, or easy to resolve. A reminder from your team may be enough when the consumer forgot a due date, missed an invoice, or needs help understanding the balance.

Limitations of In-House Collections

The main limitation is capacity. Collection work requires consistent outreach, documentation, compliance awareness, dispute handling, payment tracking, and follow-up. When your A/R team is already stretched thin, overdue accounts may not get the attention they need.

There is also a technology gap. Many internal teams are working from spreadsheets, basic billing software, or systems that weren’t designed for collection workflows. Without the right tools, even a hardworking team can struggle to identify which accounts need immediate action and those that need a different recovery path.

Benefits of First-Party Agency Support

First-party agency support gives you professional collection infrastructure while keeping the consumer-facing experience tied to your organization’s name. That can help preserve familiarity while improving consistency.

Our team can support early-stage recovery with structured communication, payment follow-up, account monitoring, reporting, and process discipline. For organizations that want to strengthen collections before accounts become seriously delinquent, this model can be both practical and reputation-conscious.

Benefits and Risks of Third-Party Collections

Third-party collections add a more formal layer of recovery. This can be valuable when accounts are older, consumers are unresponsive, balances are more difficult to recover, or internal follow-up has reached its limit.

A qualified agency brings dedicated recovery professionals, compliance oversight, skip tracing resources, payment systems, and reporting tools. Our team also understands that results can’t come at the expense of your reputation. Summit’s consumer-focused philosophy is built around preserving human dignity (P.H.D.) while helping clients recover what they’re owed.

The risk comes from choosing the wrong partner. Poor communication, aggressive tactics, confusing fees, or weak compliance controls can create complaints and reputational damage. An agency’s values, training, transparency, and track record matter as much as its recovery rate.

Legal and Regulatory Considerations

Debt collection is heavily regulated, and the rules governing consumer accounts are far more complex than many businesses realize. Whether collections are handled internally or outsourced to an agency, compliance failures can create financial, legal, and reputational consequences.

Federal Laws That Shape Consumer Collections

One of the most important laws governing third-party debt collection is the Fair Debt Collection Practices Act. This federal law establishes rules around how and when consumers can be contacted, what disclosures must be provided, and which collection practices are prohibited.

The FDCPA restricts behaviors such as harassment, misleading statements, repeated excessive calling, and communication at inappropriate hours. It also gives consumers the right to dispute debts and request validation of account information.

State-Level Compliance Requirements

In addition to federal law, many states have their own consumer protection regulations governing debt collection activity. These laws may address licensing requirements, communication restrictions, statute of limitations rules, interest limitations, and legal disclosure obligations.

Because collection laws vary by jurisdiction, businesses operating across multiple states often face a complicated compliance environment. What’s allowed in one state may create legal exposure in another.

Professional collection agencies typically invest heavily in compliance systems, staff training, call monitoring, and regulatory updates to manage these evolving requirements because the environment is too complex to manage casually.

Why Compliance Directly Affects Brand Reputation

Collection conversations are sensitive. Even when a balance is valid, the way the conversation is handled can shape how a consumer feels about your organization afterward. A careless tone, confusing message, or poorly timed contact can damage trust quickly. Today’s consumers frequently share negative experiences online through reviews, complaints, and social media.

This is why many businesses prioritize agencies that combine strong compliance standards with respectful communication strategies. Ethical recovery practices not only reduce legal risk but also help preserve customer dignity and long-term brand trust.

For agencies like Summit, this consumer-focused philosophy is central to our recovery processes, emphasizing professionalism, respect, and relationship preservation along with financial recovery goals.

Impact on Credit Scores

Collection activity can significantly affect a consumer’s credit profile, but the impact depends on how the account is handled and how long the debt remains unpaid.

When Collections Affect Credit Reports

Missed payments can appear on a credit report before an account ever reaches collections. Once a debt moves into a more formal collection process or is reported as delinquent, the negative impact often becomes more serious. Collection accounts may lower credit scores, affect borrowing ability, and remain visible to lenders for years, depending on the credit bureau and applicable regulations.

Some industries, including healthcare, now face additional reporting requirements and waiting periods before medical debt appears on consumer credit files. That is why credit impact should always be managed carefully and with compliance in mind.

How This Helps

Third-party collections can motivate people to make faster repayments because of the impact of credit bureau reporting and their structured recovery programs. For businesses and organizations, this creates a balance between encouraging payment accountability and maintaining compliant, ethical recovery practices.

Technology and Best Practices in Debt Collection

Modern collection work depends on both technology and judgment. Software can organize the process, but people still determine whether the communication is clear, fair, and productive.

How Technology Improves Recovery Efforts

Collection agencies now use advanced account management systems to organize communication, track payment activity, monitor compliance, and prioritize accounts based on risk and recovery likelihood. Digital payment portals, automated reminders, and secure consumer communication channels can also improve response rates by making repayment more convenient.

Technology also makes collections easier for your company to manage first- and third-party collections. We provide a client portal, for example, that allows our partners to monitor and upload accounts, among other capabilities, anytime, from anywhere in the world.

Why Human Communication Still Matters

Technology can make collections more efficient, but it cannot replace respectful conversation. Consumers are more likely to engage when they understand the balance, feel heard, and have a realistic way to resolve the account.

Best practices include accurate documentation, clear payment instructions, consistent follow-up, dispute management, flexible resolution discussions, and careful compliance oversight. The strongest collection programs use technology to support better human communication, not to replace it.

Choosing the Right Collection Strategy

Picking a collection strategy is often less about choosing one method permanently and more about aligning recovery with business risk, customer behavior, and operational efficiency.

Matching Strategy to Account Type

Lower-balance consumer accounts may benefit from high-volume digital outreach and self-service payment options, while larger balances need more personalized communication and negotiation.

Industries also face different collection realities. Healthcare collections may prioritize patient sensitivity and insurance disputes, while unpaid commercial lease collections may focus on lease timelines, move-out balances, or skip tracing challenges.

Look Honestly at Your Internal Capacity

Many businesses underestimate the administrative burden tied to collections. Documentation requirements, dispute handling, compliance monitoring, and consistent follow-up all require time and infrastructure.

A strategy that works for a company with a dedicated receivables department may not work for a smaller organization with limited staffing. In many cases, the most effective approach is the one that can be executed consistently without disrupting day-to-day operations.

Transitioning Between Collection Approaches

Moving an account from in-house follow-up to first-party support or third-party collections should be handled carefully. A messy transition can create confusion, disputes, and lost recovery momentum.

Avoiding Gaps in Consumer Communication

Consumers should not receive conflicting instructions, outdated balance information, or duplicated messages from multiple teams. Before an account transitions, the agency should have accurate account details, payment history, dispute notes, contact records, and any special handling instructions.

Clean handoffs protect everyone. They help consumers understand what to do next, help the agency communicate accurately, and help your organization maintain control over the recovery experience.

Keep the Process Strategic

The transition point is also a chance to reassess the account. Is the consumer still reachable? Has there been a dispute? Is the balance documented properly? Would first-party support still make sense, or is third-party placement now the better option? A good collection strategy keeps adjusting as new information becomes available.

The Bottom Line

Consumer collections work best when businesses stop seeing recovery as a one-size-fits-all process.

The most effective strategies balance timing, communication, compliance, and customer behavior rather than relying on pressure alone. Whether accounts are handled internally or through a collection agency, professionalism matters at every stage.

We help businesses recover consumer debt through ethical, results-driven collection strategies designed to protect both cash flow and long-term brand reputation. Reach out for a free consultation.

FAQs

What is the difference between in-house, first-party, and third-party collections?

In-house collections are handled by the creditor’s own staff. First-party collections can involve an agency working in the creditor’s name, so communication appears to come from the original business. Third-party collections happen when an agency communicates in its own name while recovering debt for the creditor.

When should a business outsource consumer collections?

A business should consider outsourcing consumer collections when internal follow-up becomes inconsistent, accounts are aging, staff are stretched thin, recovery technology is limited, or compliance demands are becoming harder to manage. Outsourcing can often be more cost-effective than asking an internal A/R team to manage every overdue account manually.

Is first-party collection the same as in-house collection?

Not always. In-house collection means the creditor’s own team is handling the work. First-party collection can also refer to an outside agency working in the creditor’s name. In that model, the creditor’s brand remains front-facing while the agency provides the process, staffing, technology, and recovery support behind the scenes.

Do third-party collections affect credit scores?

They can. If a collection account is reported to credit bureaus, it may negatively affect a consumer’s credit score and borrowing ability. The impact depends on the type of debt, reporting practices, account age, payment history, and applicable credit reporting rules.

What should your organization look for in a collection agency?

Look for strong compliance controls, transparent fees, respectful communication, secure technology, industry experience, clear reporting, and a proven commitment to brand preservation. The right agency should improve recovery without creating unnecessary risk for your customers, staff, or reputation.